How to get more than policy limits in a California car accident settlement

There are five standard answers to this question, and four of them are about finding money somewhere other than the at-fault driver’s auto policy. The fifth is about how his insurance company behaved.

All five run into the same problem first, and almost nobody mentions it: in California, you generally do not know what the policy limits are. Not at the start, not during negotiation, and not until a lawsuit is on file.

Key Takeaways

- Recovery above the at-fault driver’s limits comes from a different policy or a different defendant. The same policy does not pay more.

- California does not require a liability insurer to tell an injured claimant what the limits are before suit is filed. They become discoverable once it is.

- Your own underinsured motorist coverage is usually the largest single additional source, and the rules for settling without forfeiting it differ depending on whether the claim is uninsured or underinsured.

- The statutory claim against the car’s owner is capped at $15,000 per person, which is now half of what the driver himself is required to carry.

- California immunizes bars that overserve adults, so dram shop recovery is not available in the ordinary drunk driving case.

Can a settlement exceed the at-fault driver’s policy limits?

Yes, though rarely out of that policy. An insurer’s promise is capped at the number on the declarations page, and no amount of negotiation moves it.

What moves is where the money comes from. Five routes:

- Your own uninsured or underinsured motorist coverage. Usually the largest additional source, and it depends entirely on what you bought before the crash happened.

- A second liable party carrying a separate policy. An employer, a rideshare company, a trucking carrier, a business, or a public entity that maintained the road.

- An umbrella policy sitting above the driver’s auto coverage. Common enough to ask about every time, and almost never volunteered.

- The driver’s personal assets. Real as a legal matter, usually thin as a practical one.

- A claim arising from the insurer’s own refusal to settle when it had a reasonable chance to. More constrained in California than most summaries suggest, and it belongs to the driver rather than to you.

Everything below is about which of those apply to a given crash, and how you find out.

Illustration

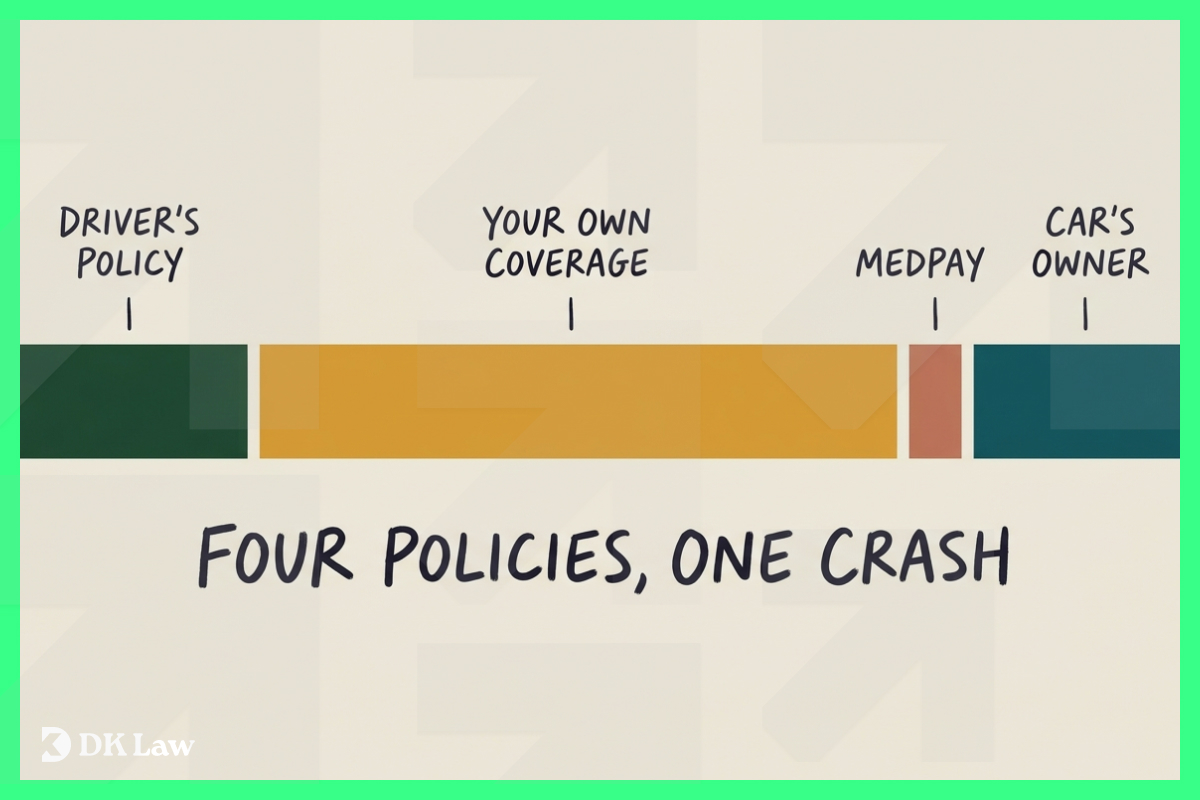

Covering $120,000 in losses when the at-fault driver carried $30,000

One policy rarely covers a serious injury. Recovery above the limit comes from stacking separate sources, each with its own rules and its own ceiling.

- At-fault driver’s liability policy — $30,000California’s minimum since January 2025. This is the only source that pays automatically, and it is the smallest one here.

- Your underinsured motorist coverage — $70,000Assumes you carried $100,000, reduced by the $30,000 already recovered. If your limits match his, this slice is $0.

- Your medical payments coverage — $5,000Pays regardless of fault. Small, immediate, and often forgotten.

- Car owner’s statutory liability — $15,000If the driver borrowed the car. Vehicle Code section 17151 caps this at half of what the driver is required to carry.

The part this chart leaves out

The $120,000 above is economic loss: bills and lost wages. Pain and suffering sits on top of it and is usually the larger number in a serious injury case, which is what pushes most claims past the policy limit in the first place.

Proposition 213 (Civil Code section 3333.4) bars uninsured drivers from recovering non-economic damages at all, even when the crash was entirely someone else’s fault. Delete that segment and many claims shrink back inside the coverage that already exists. The exception: the bar does not apply if the driver who hit you was convicted of DUI.

Figures are a hypothetical illustration chosen to show how sources stack, not an estimate, average, or prediction. Every case turns on its own coverage, injuries, and liability. Prior results do not guarantee a similar outcome.

Why are you negotiating without knowing the number?

Nothing in California law requires the other driver’s insurer to tell you how much coverage he bought.

The Fair Claims Settlement Practices Regulations govern how insurers must handle third-party claims and require a written explanation when a claim is denied or disputed. Nothing in them requires disclosure of limits. An adjuster who declines to tell you is following the rules.

Cross the state line and the answer inverts. Florida requires a liability insurer to state the coverage limits under oath within thirty days of a written request, including every insured and any coverage defense the company intends to raise. Same question, opposite answer, one border away.

The practical effect in California is that early negotiation runs partly blind. You may be arguing about whether a $45,000 offer is reasonable without knowing whether the ceiling is $50,000 or $500,000. Insurers frequently do volunteer limits, particularly when the limit is low, and disclosure ends the discussion. When they do not, you need a different tool.

How do you find out what coverage exists?

Two mechanisms. Which one is available to you depends on whether a lawsuit has been filed.

1. After filing: formal discovery. Code of Civil Procedure section 2017.210 makes the existence and contents of any insurance agreement discoverable, including the carrier’s identity and the nature and limits of the coverage. The Judicial Council’s standard form interrogatories cover it, and they reach excess and umbrella coverage too. Disclosure alone does not make the insurance admissible at trial, which removes the usual objection to asking.

2. Before filing: a time-limited demand. Code of Civil Procedure section 999, effective January 2023, applies to represented claimants and sets out what a valid demand has to contain and how long the insurer must be given, which is at least thirty days for a demand served by email or certified mail and thirty-three by regular mail. A demand that ignores the statute will not do the work later, so the formalities are the substance rather than a technicality.

Beyond the paperwork, coverage sometimes turns up through facts nobody thought to check. Whether the driver lives with a relative whose policy covers resident household members. Whether he was driving someone else’s car with permission, which can bring the owner’s policy into play. Whether an umbrella policy was purchased alongside the homeowner’s coverage, which is common enough to be worth asking about every time. Sorting out which policy responds first is its own question, and we walk through it in whose insurance pays after a California car accident.

So how do cases settle before anyone files suit?

Most of them do, which seems to contradict everything above. Three things reconcile it.

Insurers often disclose limits without being forced to, and a low limit is when they are quickest about it. Confirming that the policy is $30,000 ends the negotiation on the insurer’s terms. Silence tends to show up in the middle range, where the ceiling might be $100,000 or $500,000 and the adjuster would rather you not aim at it.

Filing suit is also less dramatic than it sounds. A large share of filed cases settle during discovery without anyone seeing a courtroom, and the complaint is often filed for the specific purpose of opening the coverage question. Settling without a trial and settling without a lawsuit are different things, and the larger recoveries people read about are usually the first kind.

The third piece reframes the question. Policy limits cap the total, not the categories. Lost wages, medical bills, and pain and suffering all come out of the same pot, so when that pot is $30,000, they compete against each other for it. Arguing over how a small pot gets divided is a much smaller opportunity than finding a second pot.

How does your own underinsured motorist coverage work?

For most people, this is the largest additional source, and whether you have it at all depends on choices made when the policy was written, which we break down in liability versus full coverage in California. The coverage itself is governed by Insurance Code section 11580.2.

A vehicle counts as underinsured only when the at-fault driver’s limits are lower than your own. Carry the same 30/60 he does, and you have no underinsured claim at all, regardless of how badly the coverage falls short of your bills. The coverage is also reduced by whatever you recover from him, so it fills a gap rather than stacking on top.

Then there is the settlement trap, and here the standard advice is wrong often enough to cost people their claims. Uninsured motorist coverage does carry a strict consent requirement, and settling with the at-fault driver without your insurer’s consent can forfeit it.

Underinsured motorist coverage works differently, because the statute requires you to exhaust the at-fault driver’s limits before the coverage responds at all. A California appellate court has held that an insurer cannot use a consent requirement to defeat a claim the statute obligates you to pursue first.

Notify your carrier either way, in writing, before you sign anything. The distinction matters, and treating both claims as though consent is absolute leaves money unclaimed.

Why is the claim against the car’s owner worth less than it looks?

When someone drives another person’s car with permission, the owner is vicariously liable. That claim comes with a cap, and the cap has not moved in a very long time.

Vehicle Code section 17151 limits the owner’s liability to $15,000 for injury to one person, $30,000 for more than one, and $5,000 for property damage. Those figures were set alongside the state’s original minimum insurance requirements in 1967 and have stayed there. The minimums went to 30/60/15 in January 2025, and the legislation that raised them amended five sections of the Vehicle Code. Section 17151 was not among them.

So the arithmetic now runs backward. The statutory claim against the car’s owner tops out at half of what the driver is legally required to carry. In any case with a real injury, that claim is close to a rounding error.

The theory that still has teeth is negligent entrustment, which is a claim about the owner’s own conduct rather than the driver’s. Lending a car to someone you knew was unlicensed, or drunk, or a documented danger behind the wheel is independent negligence, and it falls outside the cap entirely. In a serious case, it is usually the only owner theory worth the trouble of pleading.

When is someone else’s business liable?

An employer answers for a driver acting within the scope of employment, which is why a crash with a plumber’s van is a different case from a crash with a plumber. Commercial policies are larger by orders of magnitude.

The scope question is where these claims are won or lost. Ordinary commuting normally sits outside the scope of employment under what California courts call the going and coming rule. The exceptions do a lot of work. A driver required to bring a vehicle to work so the employer can use it during the day, or running an errand for the employer on the way, or traveling to a business function, can all fall back inside. Whether the employer got some benefit from the trip on the day of the crash tends to decide it.

Rideshare crashes turn on timing. Public Utilities Code section 5433 requires a transportation network company to carry $1,000,000 in primary liability coverage from the moment the driver accepts a ride request until the trip is complete. Before acceptance, while the app is merely running, the required coverage is far smaller. Whether the driver had accepted a request thirty seconds before impact can change the available coverage by a factor of twenty, which is why the app data matters more than the police report in these cases. Our rideshare claim timeline covers how that record gets preserved.

Commercial trucks carry federally mandated minimums well above anything required of a passenger car, starting at $750,000 for general freight and rising for hazardous cargo. Beyond the carrier, the broker who arranged the load and the company that hired an unfit driver can be separate defendants with separate coverage.

What if a government entity is responsible?

A public entity can be liable for a dangerous condition of its own property, which covers badly designed intersections, missing signage, unrepaired road defects, and obscured sightlines. Recovery from a city, county, or Caltrans is not capped the way a private minimum-limits policy is.

Two things make these claims difficult. Design immunity protects a public entity where a responsible official approved the design in advance, and it defeats a large share of roadway claims outright. And the deadline is brutal: Government Code section 911.2 requires a written claim within six months of the injury, not two years.

A viable claim against a public entity can expire while the ordinary auto claim still has eighteen months to run, and by the time most people start asking whether the road was the problem, the six months is gone.

Which sources sound available but usually are not?

Two worth naming, because both circulate widely as options and neither works the way people expect.

Serving alcohol to an adult who then causes a crash creates no civil liability for the bar or restaurant in California.

Business and Professions Code section 25602 treats consumption rather than service as the cause of the resulting harm, and the immunity is broad. The narrow exception covers a licensee who serves an obviously intoxicated minor. In the ordinary drunk driving case, the bar is not a defendant, whatever you have read elsewhere.

The at-fault driver’s personal assets are the other one. The claim is real, and a judgment is enforceable, but people who carry minimum coverage are often in a similar financial position, and California exemptions shield a meaningful portion of what they own.

What does Proposition 213 do to the math?

If you were uninsured when the crash happened, Civil Code section 3333.4 bars you from recovering non-economic damages. Medical bills and lost wages survive. Pain and suffering does not, even where the other driver was entirely at fault.

That guts the premise of this whole exercise for the people it applies to, because non-economic damages are usually most of what pushes a claim past the policy limits in the first place. Strip them out, and the claim often fits inside the coverage that already exists.

The exception is worth knowing and gets left out of most discussions of the statute. The bar does not apply where the driver who injured you was convicted of driving under the influence. In that situation, an uninsured plaintiff recovers non-economic damages like anyone else.

Common questions

Can I recover from more than one policy for the same crash? Yes. Multiple defendants with separate coverage, and your own underinsured motorist coverage layered behind the at-fault driver’s, are both routine.

Does hiring a lawyer make the policy bigger? No. What changes is whether the additional policies and defendants get identified before the deadlines pass, and whether the paperwork you sign preserves them.

How do I find out if the driver has an umbrella policy? Ask, and expect nothing. It becomes discoverable once suit is filed.

What if the at-fault driver had no insurance at all? Different analysis, driven mostly by your own coverage. See what an uninsured driver settlement looks like in California.

Find out what is actually available in your case

The ceiling on a car accident claim is usually set by facts nobody has checked yet. Who owned the car, who employed the driver, what the app was doing, whether a public entity maintained the road, and what coverage exists that no one has volunteered.

Contact DK Law for a free consultation.

Prior results do not guarantee or predict a similar outcome in any future case. Attorney Advertising. DK Law, Costa Mesa, CA.

DK All the way

From Your Case to Compensation, we take your case all the way.

Schedule a Free Consultation

Get Expert Legal Advice at Zero Cost.

At DK Law we’re with you – all the way.

Get a Free Consultation with our experts today!